New Zealand-based Master of Wine, freelance wine writer and wine judge Emma Jenkins endeavours to find out why sales of New Zealand wine in the US are performing better than their Australian counterparts.

Trans-Tasman rivalry is an enduring feature of Australia and New Zealand’s relationship, a (mostly) friendly tug-of-war played out in sports, politics and bad jokes. When it comes to wine industries, New Zealand is very much the younger, smaller sibling, however it is also the one punching well above its weight in the sought-after United States market.

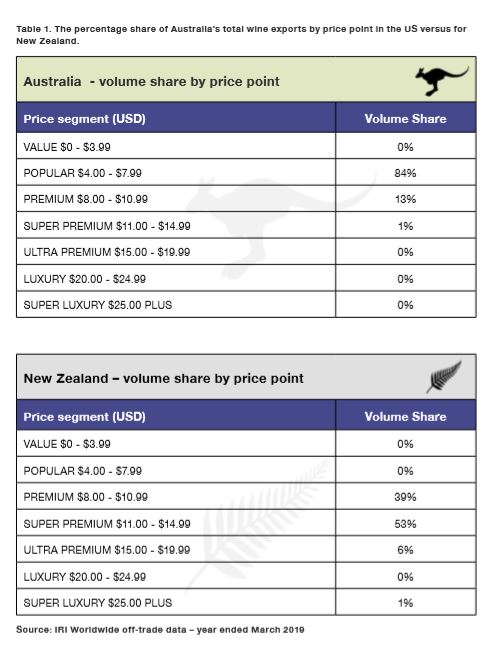

New Zealand’s US wine exports boast an average value per litre of NZ$7.17 (AU$6.75) compared to Australia’s AU$2.66, growing 3% in volume and 4% in value in 2018. In the same period, Australia’s US exports decreased 17% by volume and 16% by value. This US decline was despite steady gains in Australia’s other top five export markets.

So what’s actually going on?

It helps to first consider the US wine market. Despite wine consumption being relatively low at around 11L per capita, it is now the largest global wine market at US$70.5b, or 408 million cases, of which US$23b/105m cases are imported. There is a clear trend for premiumisation: most growth has been in the US$10+ segment with the total market value increasing 5% in 2018 while volume rose by just 1%.

However, for importers the US’s complicated three-tier distribution system, a legacy of prohibition which varies not only from state to state but often county to county, can prove very difficult to navigate. Securing reliable distribution channels is vital, no matter what size or shape the brand.

Australia exports around 60% of its wine, enjoying a long and largely successful history in the US, however the current US consumer perception of Australian wine is predominantly value-for-money rather than fine/expensive wine. The ‘sunshine in a bottle’ era followed by the explosive and enduring success of ‘critter wines’, such as Yellowtail (current annual US sales are around 10m cases), has reinforced the image of fruity, commodity wines.

Of course, this is far from true but in the minds of the US consumer the reality lags considerably behind the cheapand-cheerful image, a legacy now being actively addressed.

“Positive perceptions of Australian wine are growing among US wine consumers,” says Hannah Bentley, communications manager for Wine Australia. “While this is not immediately reflected in sales, it helps us assess the changing attitudes and provides insights as to where the opportunities are in the market. Premiumisation is a trend that we are following closely and are leveraging opportunities for Australian wine companies to build on.”

Working with the Australian Government’s AU$50m Export and Regional Wine Support Package, Wine Australia is focussed on shifting the message via initiatives such as Australia Decanted, a four-day wine education program for 100 key influencers, and September’s Aussie Wine Month.

The message seems to be gaining traction. California-based writer for jancisrobinson.com Elaine Chukan Brown comments, “Australia has a lot of quality wines to please the wine geek community. Wine Australia has made an enormous marketing push in the last few years and it’s having an impact on trade awareness but I don’t believe it is penetrating the broad consumer. That said, brands like [Treasury Wine Estate’s] 19 Crimes are helping to switch things up in the consumer market.”

An edge for Australia?

It’s here that Australia may gain the edge. New Zealand’s production and exports are all about one grape, one region: Marlborough Sauvignon Blanc. Some 77% of NZ’s production is Sauvignon Blanc, of which 85% comes from Marlborough.

At NZ$1.7b per annum and 85% of production, exports are at a 10-year high. The US edged past the UK as the number one market in 2016; its 72m litres are considerably more lucrative at NZ$521m versus the UK’s 74m litres/NZ$386m.

New Zealand wines are now ranked 7th for volume and 3rd for value in the US; 94% is Sauvignon Blanc, with the vast majority just a handful of brands, for as one Marlborough producer says, “The US consumer loves a market leader: ‘If I can drink Kim Crawford, why do I need anything else?’”

This has made ‘New Zealand Wine’ an easy message for consumers to grasp, but it’s come at a cost of market awareness of NZ’s other styles. Chukan Brown adds, “The big thing for NZ success has been the insane market command of Sauvignon Blanc as an unquestioned, recognisable style. Australia doesn’t have a strong category driver like that in the US at this point. But it isn’t clear that NZ has been able to leverage that in any large scale to benefiting other categories, though there are small-scale inroads of interest for geeky wines. The downside of how NZ has grabbed the US market is that if/as interest in Sauvignon wanes, so does NZ’s hold on the market share.“

It’s a dynamic echoed by Joe Czerwinski, managing editor at the Wine Advocate, who observes, “The big difference between Australia and New Zealand is that one projects an image of inexpensive, mass-market wine, while the NZ brands have managed to hold pricing reasonably firm with a more upmarket message. The high visibility of the big brands is what drives the general perception.

“I think when you drill down further, and talk to more wine-savvy consumers, retailers and sommeliers, the picture is more complex. Australia, given its greater size and diversity of wine regions/ styles, is probably seen as more cutting edge and interesting. At least from what makes it into the market here, there are more experimental and natural wines to grab young consumers’ interest.

“New Zealand, on the other hand, is struggling to gain market share in areas other than Sauvignon Blanc. Yes, the Pinot Noirs can offer an alternative to domestic versions, but they’re not all that common on retail shelves or restaurant wine lists. Varieties other than these are largely still rarities that consumers have to actively seek out,” Czerwinski said.

Both Australian and NZ producers have to contend with the reality of a handful of very large companies selling the vast majority of labels gracing US shelves. But NZ’s smaller production (2018 crush was 419,000 tonnes to Australia’s 1.79m) eventually shows its hand. While NZ may never risk treading Australia’s rocky path of low value/large volume, NZ producers’ fundamentally boutique scale means even when a toehold in distribution is secured, it can be difficult to supply required volumes — and presence in the market place is all.

Marlborough winemaker Ben Glover (Zephyr) asks, “Is NZ physically big enough to supersede and maintain something bigger than [1m case] Kim Crawford? Probably not … we may have hit our ceiling as to how we navigate the US with a branded base.”

Broadening the NZ offer

To broaden the offer, NZ Winegrowers runs an extensive program for trade, media and consumers, last year presenting 1200 different wines across 35 events throughout the US. New Zealand’s sustainability message (98% of wines are Sustainable Winegrowing NZ accredited) is increasingly welcomed.

Chukan Brown notes that “notions of premium wine have gotten wrapped up with ideas of sustainability too, so that it isn’t just a price category question any more. Nielsen was able to show that around a third of consumers are willing to pay more for organic and sustainable products, including wine. NZ has done a far better job at marketing around this idea.”

Tourism supports the message, with 27% of NZ tourists visiting a winery and many more drinking NZ wines.

Arguably Wine Australia’s greater focus has been on mainland China which represents 33% of its exports (compared to US’s 18%), a booming market whose strong preference for red wine NZ finds trickier to satisfy, but the US is clearly territory with potential to lift value while not necessarily sacrificing volume.

Wine Australia’s Bentley is keen to make the point that, “In our export data, we are seeing rising numbers for varieties such as Fiano and Grenache. While this is off a small base, it is interesting to note that when presented at our seminars and trade tastings in the USA these wines generate significant excitement about the diversity offered in Australian wines.”

Throw in the constantly shifting sands of currencies, Free Trade Agreements (has there ever been a more volatile time in US politics?), whims of somms and gatekeepers, the legalised marijuana disruptor (there’s good reason why Constellation recently invested US$4b into a Canadian cannabis company), boxed and canned wines shaking off their downmarket image as millennials engage with wine in a completely new fashion, the ever-changing landscape of e-commerce, premiumisation, consolidation…the US represents plenty of scope for value growth but it’s a longterm game.

New Zealand may seem to be beating its neighbour but the reality is both countries are fighting similar battles. While it is unlikely there will be much love lost in competition for shelf space, building the message of Antipodean quality, depth and diversity clearly remains the best way forward for both.

This article was originally published in the July issue of Australian & New Zealand Grapegrower & Winemaker magazine. Click here to subscribe.